Topgolf Callaway Brands: Can Investors Score a Double Eagle?

Ticker: MODG ⛳

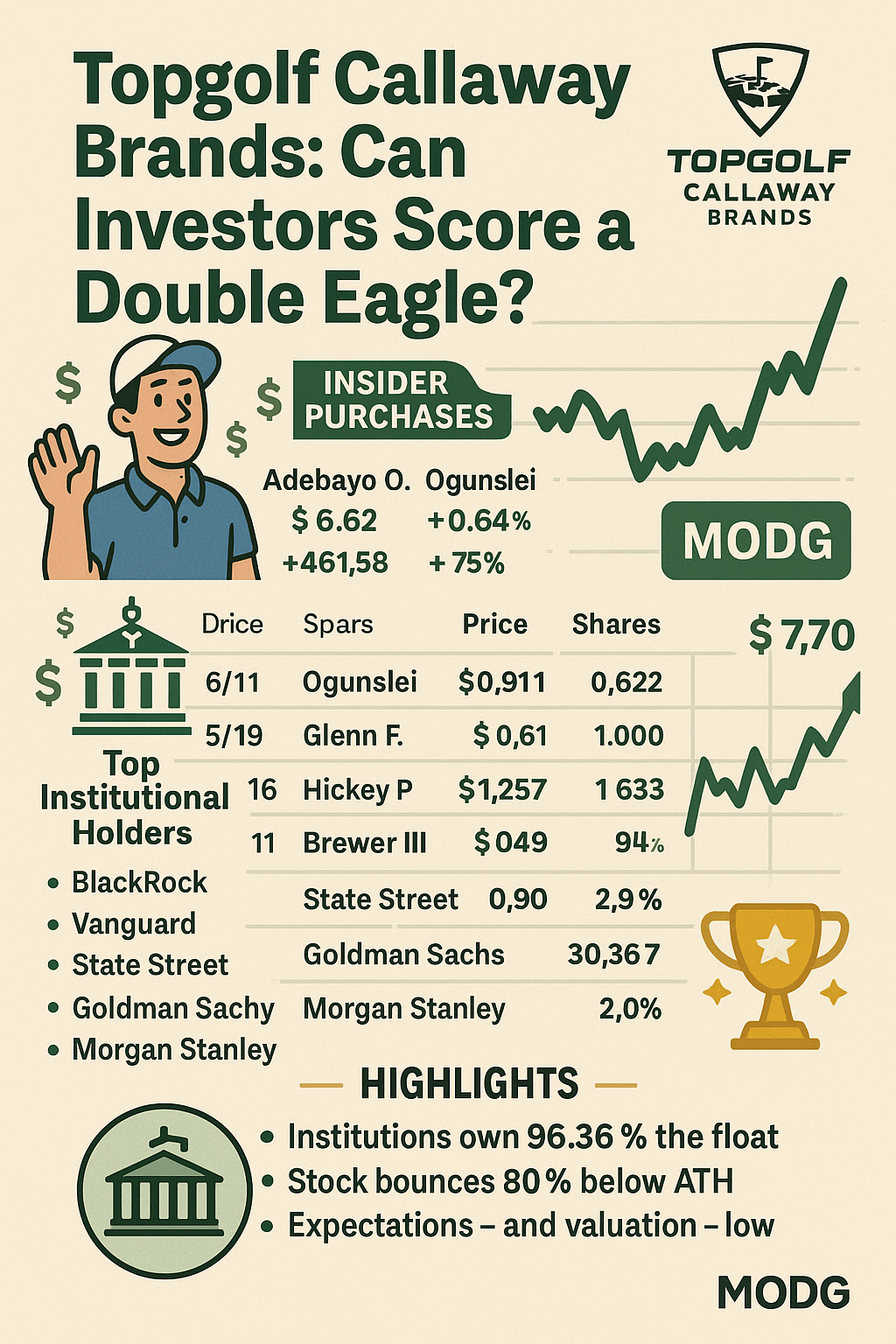

Price: $7.70 (+4.19%, as of June 10, 2025)

Trigger: 📌 Multiple insider purchases, institutional support, and signs of a business turnaround.

📥 Big Insider Buys = Big Belief?

Adebayo Ogunlesi (Director) just doubled down like a Tour pro:

-

June 6: +461,583 shares @ $6.62 = $3.06M

-

June 4: +383,701 shares @ $6.47 = $2.48M

Other insiders joining the clubhouse: -

🏌️♂️ Glenn Hickey (EVP): 10,000 shares

-

👔 CEO Oliver Brewer: 20,000 shares

-

🧢 Director Russell Fleischer: 30,000 shares

These aren't putt-putt purchases. This is a serious bet on the company's direction. 🤑

🏦 Institutional Power Play

Institutions hold 96.36% of the float. That includes:

-

BlackRock (12%)

-

Providence Equity (11.5%)

-

Vanguard (7.9%)

-

Goldman Sachs, Morgan Stanley, and more.

When the big guys stay on the green, retail investors might want to bring their clubs. 🏌️♀️📊

🔍 For full Institutional Ownership breakdown, see here.

📊 Q1 2025 Results: A Mixed Bag, But Signs of Stabilization

-

💰 Net revenue: $1.09B (down 4.5% YoY — but above expectations)

-

📈 Adjusted EBITDA: $167.3M (+4.0%)

-

🧾 Non-GAAP EPS: $0.11 (vs. $0.08 in Q1 2024)

-

💳 Available liquidity: $805M (up 12%)

-

🎯 Jack Wolfskin sale in progress, Topgolf separation planned

CEO Chip Brewer: “We met or beat plan in all segments.” Translation? ⛳ Better than feared.

🚨 Segment Breakdown

Topgolf:

-

Revenues down 12% at same venues

-

Losses reduced via cost cuts

-

Separation on deck = 🔄 strategic reset

Golf Equipment:

-

Revenue down slightly due to FX & fierce competition

-

💥 Operating income up $19.5M thanks to cost control & margin improvement

-

🏆 Elyte Driver winning awards

Active Lifestyle:

-

Revenues down due to Wolfskin resizing in Europe

-

💪 Operating income up $5.9M, China still growing

👉 Want the full picture? Dive into Topgolf Callaway Brands’s financials here.

📉 Still Below Par… But Value in the Rough?

Let’s not sugarcoat it:

-

📉 Shares are down 80% from the $37.75 ATH (2021)

-

🧾 Net income this quarter = $2.1M

-

🏚️ Still rebounding from a massive $1.45B goodwill write-off in 2024

-

💸 Price/Sales: 0.32 | Price/Book: 0.56 | EV/Revenue: 0.94 → That’s… cheap.

The company may be described as mid-swing in a turnaround.

⛳ 5 Bullish Signals

-

Insider Buying: Consistent, large, and confident

-

Institutional Support: Wall Street’s still playing this round

-

Turnaround Strategy: Cost cuts, asset sales, separation of Topgolf

-

Liquidity Is Up: $805M available = breathing room

-

Valuation: Deep value metrics… if results improve

😬 5 Risks to Keep in Play

-

Revenues & profits still under pressure

-

Consumer softness + tariffs = headwinds

-

Restructuring not yet done

-

Growth story unclear until Topgolf separation lands

-

Insider bets don’t always pay off 🃏

Interested in another investment idea?

Check our take on UnitedHealth Group.

🦅 So... Can MODG Score a Double Eagle?

A double eagle (albatross) is a near-mythical golf score: 3 under par on one hole.

And while MODG shares might not hit that miraculous shot anytime soon…

A birdie? Maybe.

An eagle? Why not?

At these levels, a swing might be worth it — especially with the pros betting behind the scenes.

🏌️⚖️ Disclaimer

We don’t play much golf.

Last time we tried, it turned into a hike.

Do your own research. Score your own game.

Invest at your own risk. 💼⛳

🧭 Want More Like This?

👉 Browse our Insider Purchases Center

👉 Explore our Follow the Pundits Hub: When Big Bets Matter

👉 Check out our Young Guns & Turnaround Stocks

👉 Dive into Stock Market Humor & Serious-ish Plays

👉 International Investment Opportunities await here.

👉 For even older brands on new missions, explore our Corporate Resurrection Series. Nope, doesn't exist anymore.

Got a thought? A tip? A tale? We’re all ears — drop it below.: