Quanterix Insiders Are Buying. Should You?

Ticker: QTRX 🧬

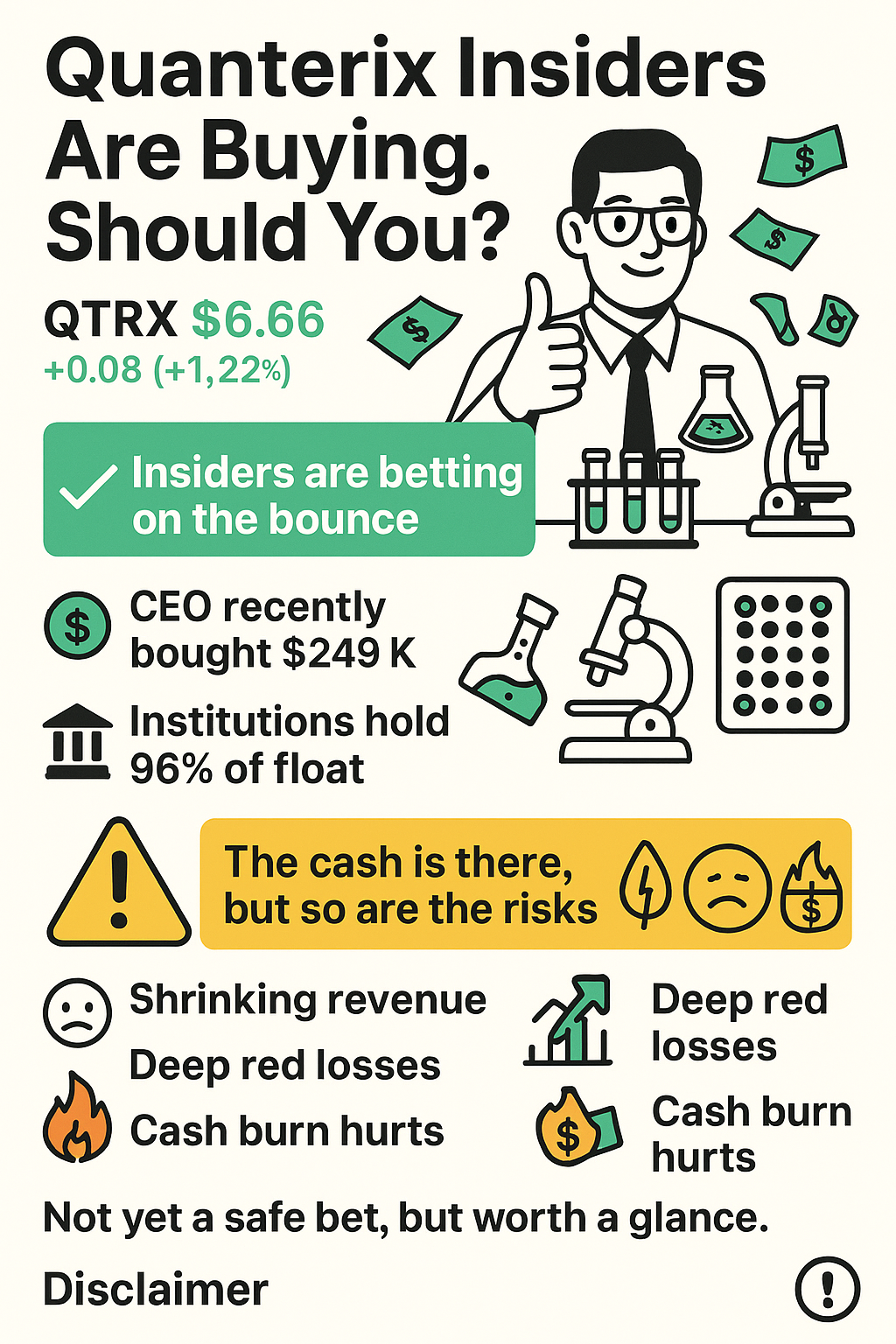

Price: $6.66 (+1.22%, as of June 11, 2025)

Trigger: 📌 CEO + directors loading up on shares = eyebrows raised.

📥 Insider Activity: Loading Up on the Dip

-

🧪 Masoud Toloue (CEO): Bought 45,900 shares → +10% position

-

🧠 David R. Walt (Director): Scooped 210,000 shares → +14%

-

💼 William Donnelly (Director): Bought 93,113 shares → +203% increase

🚨 That’s real money hitting the table — not just pocket change. Total: over $1.8M invested in less than a week.

🧱 Institutional Support: Strong Like a Protein Bond

Institutions own a whopping 96.77% of the float.

Top holders include:

-

Ameriprise (9.57%)

-

BlackRock (7.91%)

-

Portolan, Vanguard, UBS, and William Blair also in the mix

🔍 For full Institutional Ownership breakdown, see here.

The smart money seems intrigued. But why?

🔬 What Does Quanterix Actually Do?

Quanterix builds futuristic-sounding machines to detect proteins at ultra-low concentrations. Think:

-

🧫 HD-X, SR-X, SP-X platforms (because biotech can’t resist cool names)

-

🧪 Services like sample testing, “homebrew” assay development (not beer), and diagnostics

-

🧠 Focus areas: neurology, oncology, immunology, inflammation

It's science-y. It’s complex. It’s headquartered in Billerica, Massachusetts. Of course it is.

📉 Q1 Financial Highlights (aka: not the good part)

-

Revenue: $30.3M (↓ 5%)

-

GAAP gross margin: 54.1%

-

Adjusted gross margin: 49.7%

-

Net loss: $20.5M (vs. $11.2M last year)

-

Cash on hand: $269.5M

-

Adjusted cash burn: $9M for the quarter (but $22M including acquisition/legal spend)

🔻 Still bleeding, but at least the wallet’s not empty.

🧾 2025 Outlook: Still in the Red, But With a Plan

-

Projected Revenue: $120M–$130M (↓ 5% to 13%)

-

Adjusted cash burn for year: $35M–$45M

-

Gross margin goal: 50–54%

-

💡 Positive cash flow projected… in 2026 (well, at least that's the hope) with a 💰 Cash balance of $100M+

Management also renegotiated the Akoya Biosciences merger:

-

Deal value slashed 67%

-

QTRX ownership now 84% post-close → could be good

And yes, they’ve launched a cost-cutting plan targeting $30M/year in savings. 🪓

👉 Want the full picture? Dive into Quanterix’s financials here.

😬 The Risks (Because It’s Not All Assays & Acquisitions)

-

Top-line erosion — revenue shrinking, not expanding

-

Net losses are growing — not shrinking

-

Cash burn is real and ongoing 🔥💸

-

External pressure — research funding cuts, biopharma slowdown, and tariffs

-

Execution risk — Will Akoya integration help or distract?

🧪 Final Take: Curious, But Handle With Gloves

✅ Pros:

-

Insiders are buying big

-

Institutions are still in

-

Positive cash balance

-

Proactive cost-cutting

-

Akoya renegotiation looks more favorable now

❌ Cons:

-

Burning cash like a Bunsen

-

Revenue decline is no joke

-

2026 cash flow goal feels far away

-

Complex tech with gear sounding like space tech (HD-X, SP-X, SR-X), but it has yet to take on the world

Verdict? Start small if you must — or just wait. Watch for momentum to improve. No need to rush the pipette.

Interested in another investment idea?

Check our take on UnitedHealth Group.

🧬 Disclaimer

We love to have fun — but losing money is not one way to do it.

🧪 This is not financial advice. Just molecular-level speculation wrapped in science-sprinkled sarcasm.

Invest at your own risk.

🧭 Want More Like This?

👉 Browse our Insider Purchases Center

👉 Explore our Follow the Pundits Hub: When Big Bets Matter

👉 Check out our Young Guns & Turnaround Stocks

👉 Dive into Stock Market Humor & Serious-ish Plays

👉 International Investment Opportunities and value plays await here.

👉 For even older brands on new missions, explore our Corporate Resurrection Series. Nope, doesn't exist anymore.

Got a thought? A tip? A tale? We’re all ears — drop it below.: