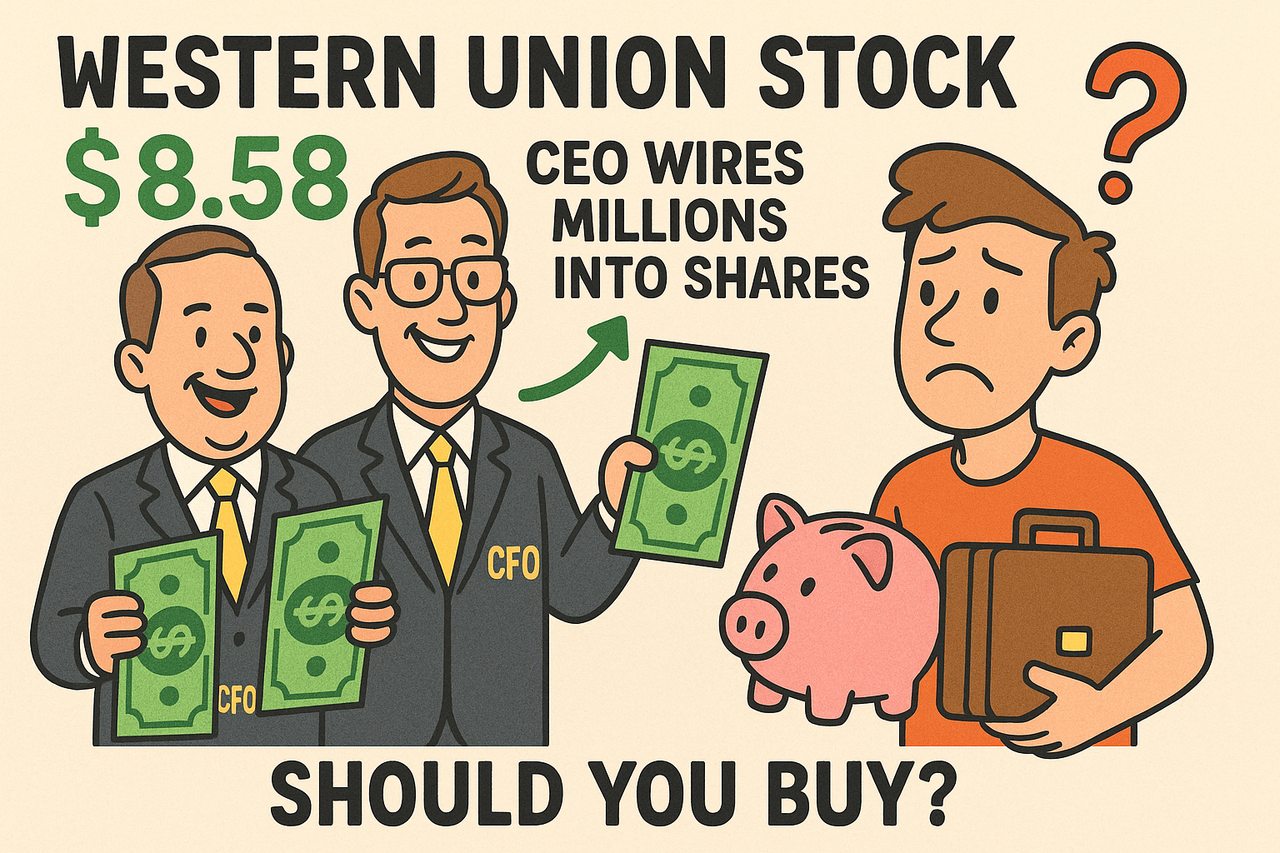

Western Union (WU): Cash Transfers, CEO Buys, and Maybe a Stock Rebound?

Price: $8.58 (+1.66%) as of Aug-26-2025 💸

🚨 Trigger: Insider Purchases (Follow the Money)

Western Union’s CEO and CFO are literally wiring money… into their own stock.

-

CEO Devin McGranahan bought 176,470 shares at $8.49 (+$1.5M).

-

CFO Matthew Cagwin bought 17,500 shares at $8.36 (+$146K).

-

Even a director was in on it last year at higher prices ($12.85).

That’s commitment — unless they accidentally hit “send” to themselves instead of Aunt Rosa in Argentina. 🏦😂

🏦 Institutions Onboard

Insiders aren’t alone:

-

Vanguard: 35.8M shares

-

BlackRock: 31M shares

-

State Street: 13.6M shares

In total, 95% of the float is held by institutions. Translation: Wall Street thinks WU is still worth more than just nostalgic yellow kiosks in airports.

Not everyone’s buying, though: short interest is 9.67%. Some traders clearly expect more “Western Downion.” 📉

For Western Union (WU)'s Institutional Ownership breakdown, 🔍 see here.

📊 Business & Financials

2024 Results

-

Revenue: $4.2B (down 3% reported, flat adjusted)

-

GAAP operating margin: 17% (vs 19%)

-

EPS: $2.74 GAAP, $1.74 adjusted

-

Returned $496M to shareholders (dividends + buybacks)

2025 Outlook

-

Revenue: $4.1–$4.2B (flat, but hey, at least not crashing)

-

EPS: $1.54–$1.64 GAAP; $1.75–$1.85 adjusted

Q2 2025 Snapshot

-

Revenue: $1.03B (down 4%)

-

Branded digital: +6% revenue, +9% transactions

-

EPS: $0.37 GAAP, $0.42 adjusted

So: stable, profitable, but not exactly setting Zelle on fire. 🔥

👉 Want the full picture? Dive into Western Union (WU)'s financials here.

💰 Valuation: Cheap or a Trap?

Some numbers are so low they look like typos:

-

P/E: 3.25 trailing, 5.0 forward (🤯)

-

Price/Sales: 0.70 (bargain bin)

-

EV/EBITDA: 2.99 (cheap-cheap)

-

Dividend Yield: ~11% (!!!)

But high Price/Book (3.14+) and weak growth suggest it might be cheap for a reason. 🧐

⚠️ Risks (a.k.a. Why It’s Not All Sunshine and Wire Transfers)

-

Declining growth: Top line is flat, profits sluggish.

-

Fintech invasion: Remitly, Wise, PayPal, and Cash App eat WU’s lunch.

-

Regulatory burdens: AML + global compliance = costly headaches.

-

Macro shocks: Currency swings, political crises → remittance drops.

In short: Western Union = safe for your money transfers, not guaranteed safe for your portfolio.

💡💡💡 Curious about another deep oil exploration play?

Check our takes on UnitedHealth Group or even Oscar Health.

🎯 The Funanc1al Take

WU is a value play: dirt cheap by valuation, still cash-flow positive, still paying a fat dividend. But it’s also a potential value trap if it can’t innovate past “money wiring, but yellow.”

So, should you invest?

-

Bull Case: CEO & CFO are buying, institutions are heavy holders, and valuation screams “bargain.”

-

Bear Case: Revenues declining, fintech rivals everywhere, and dividend cuts loom if profits slide.

👉 Western Union may still move your money — the question is whether it can also move its stock.

⚠️ Disclaimer:

We wire jokes, not financial advice.

We laugh, we analyze, we meme. We just sell jokes and opinions — and yes, we’re billing your sense of humor. 🎪💸

We’re not financial advisors. We’re FUNancial advisors.

Turbulence ahead? Invest at your own risk, always DYOR, hold the FOMO, and don’t invest what you can’t afford to lose.

🧭 Want More Like This?

- 🕵️ Insider Purchases Center

- 📣 Follow the Pundits Hub

- 📈 Young Guns & Turnaround Stocks — Track More Growth (and Growing-Pain) Plays

- 😆 Stock Market Humor & Serious-ish Plays

- 🌍 See the world differently and check out more international market picks and fun takes. Explore International Investment Opportunities and value plays 💸 Cheap Stocks with (Maybe) Big Upside

- 🧟 Corporate Resurrection Series — Our special series on companies rising from the financial grave. 🎯 The “Turnaround or Toast” Series (If it still exists. We’re not sure. Ask the intern.)

- 📈 Biotech Bets & Innovation Radar (Problem is we can't detect the Radar)

😂 Laugh, Learn, Invest: funanc1al.com | Funanc1al: Where Even Finance Meets Funny

Got a thought? A tip? A tale? We’re all ears — drop it below.: