Vail Resorts (MTN): A Powder Day for Your Portfolio? Or a Slippery Slope? 🎿💸

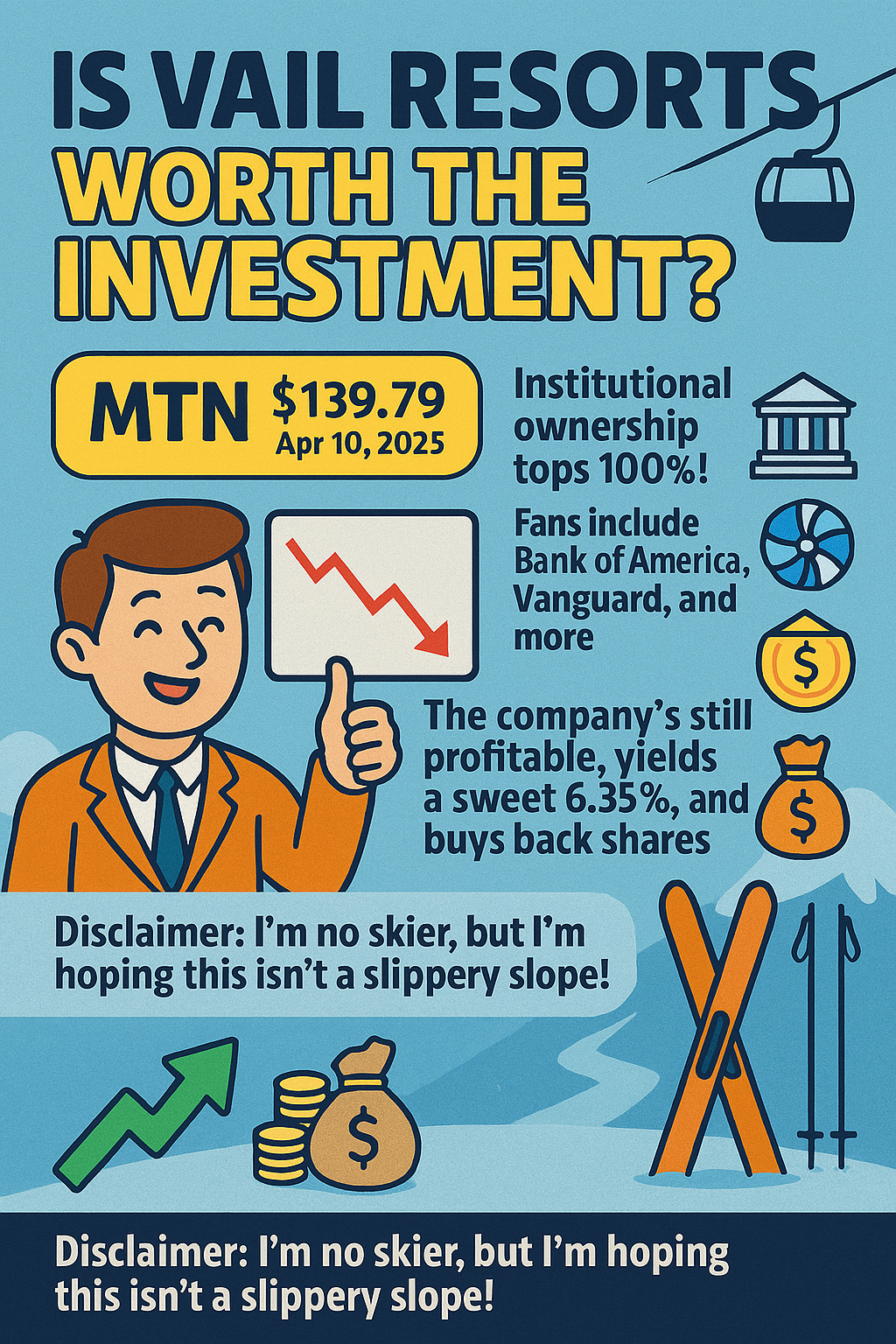

As of April 10, 2025 - Vail Resorts (MTN) | $139.79

Let’s talk about Vail Resorts (MTN) – what if the ski giant suddenly is as much about your investment portfolio as it is about the slopes? Are these investors on a smooth ride, or is Vail’s stock just a black diamond downhill? 🤔 Let’s break it down and see if it’s a sweet spot for your portfolio—or if you’ll be slipping and sliding! ❄️🏔️

🏔️ Why So Many Investors Are Shredding for Vail

First off, Vail's institutional ownership is through the roof—but not in the way you might think. With 111% of its shares owned by funds, it’s like buying Vail stock means you are a fund! Why? Well, it’s all due to the quirky world of short sellers and reporting delays. But hey, who can argue with Bank of America owning 15%, and other giants like Vanguard, BlackRock, and Capital International Investors owning around 9% each? That's some serious confidence in those ski slopes! 🏦💰

🎿 Insiders: Not Much to See, But a Little Glimmer

Insiders have been a bit quiet—no dramatic buying or selling. But there is a silver lining! Vail's CFO, Angela Korch, has made small buys over the past year (about $160k in total at a price ranging from $160 to the mid-$170s). So, if anyone knows where this company is headed, it’s probably her. Could it be a good omen? Maybe! ⛷️

📉 From Peaks to Valleys: The Stock’s Wild Ride

Here’s the lowdown: Vail Resorts hit a peak of $376.24 per share in November 2021. But since then, it’s taken a nosedive, losing about two-thirds of its value. Ouch. But recently, the stock has been trying to show signs of life, bouncing back from a 5-year low of $129.85. The overall market is bearish, which sure doesn't help! Still, could this be the start of a bullish comeback? Let’s find out! 📈🎢

💰 The Financials: Not Too Shabby!

In Q2 FY 2025, Vail posted net income of $245.5 million (up from $219.3 million last year) and EBITDA of $459.7 million, showing an 8% increase. The resource efficiency transformation plan is expected to bring $100 million in savings annually by 2026. Throw in a 6.35% dividend yield and a share buyback worth $20 million, and it seems like Vail isn’t just skiing by—it’s sliding toward profitability! ❄️💸

⛷️ Vail's Top-Line Story: Slow and Steady Wins the Race

Vail isn’t exactly going to break the sound barrier in terms of growth. Sales have been increasing by just 3-5% year-over-year. Not blazing fast, but steady—kind of like a well-practiced skier. ⛷️ So, if you’re looking for explosive growth, this might not be your powder day. But if you want something steady and reliable, Vail could be the lift ticket you need. 🎟️

🏔️ Key Takeaways:

-

$100 million in cost savings by 2026 – they’re trimming the fat.

-

6.35% dividend that’s as steady as a well-packed ski slope. Share repurchase program – Vail is buying back shares at a decent clip.

-

As of January 31, 2025, the Company's total liquidity was approximately $1.7 billion. This includes $488 million of cash on hand. Net Debt was 2.5 times its trailing twelve months EBITDA. The balance sheet is healthy.

- The company has a P/E ratio of 20.5, so it's not outrageously expensive, but it's not exactly cheap either.

🎿 Risks You Should Keep in Mind:

-

Slow Revenue Growth: 3-5% is decent, but it’s not exactly going to the moon. 🚀

-

Weather Dependence: Snowstorms, blizzards, tsunamis, or the lack of them could make or break a ski season. Don’t even get us started on strikes! ❄️❄️

-

Competition: With plenty of other resorts around, Vail can’t rest on its slopes. Innovation is key! 🏔️

🏞️ Is Vail the Right Investment for You?

Here’s the deal: Vail Resorts isn’t booming like a powder day after a fresh snowfall, but it’s also not a wipeout. If you’re after steady dividends, a solid balance sheet, and cost-saving measures that could lead to long-term growth, Vail might just be a great fit for your portfolio. But if you’re looking for something with more zip (like a quick jump from one slope to the next), Vail might not be your high-flying stock. 🎿📊

🎿 Final Thoughts:

Don’t expect this stock to be the next big thing, but it’s no slush pile either. With its solid dividends, $100 million in cost savings coming down the slope, and a healthy balance sheet, Vail Resorts could be a safe bet for investors who want stability with a little bit of ski-lift fun. 🏔️

So, will investing in MTN be a smooth ride down or are we heading for a slippery slope? You’ll have to decide. We’re hoping for a sweet descent! 🎿💸

Disclaimer: This is not financial advice. Always do your research and consult your financial advisor before making any investment decisions. If you end up in a wild ride or face a bad snowstorm in your portfolio, please don’t blame us, and remember, we’re hoping investing in MTN is no slippery slope! 😜

Got a thought? A tip? A tale? We’re all ears — drop it below.: