This Wound Care Stock Doesn't Have to Hurt! 🩸🩼

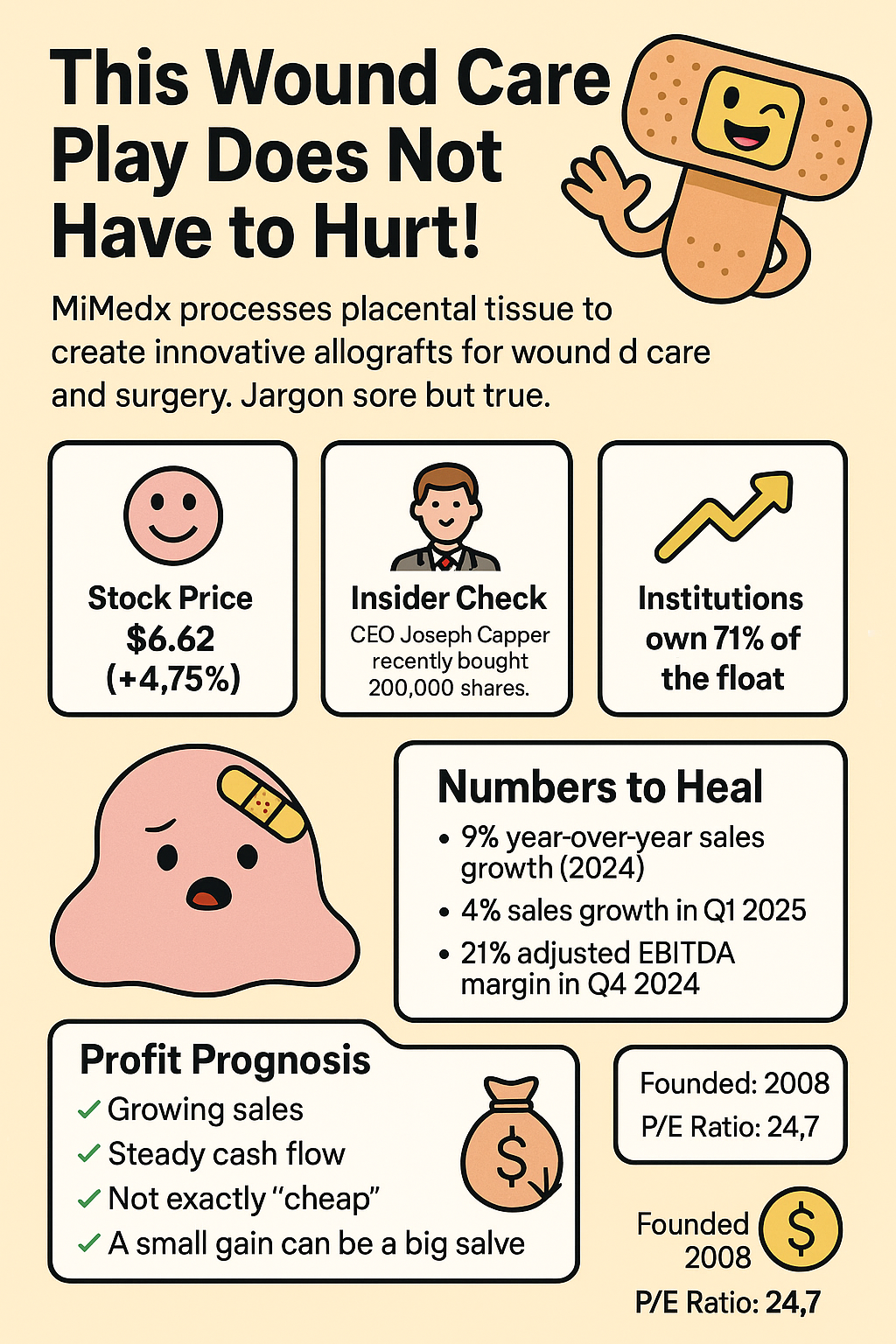

Stock Spotlight: MiMedx Group (MDXG, $6.62, +4.75%)

MiMedx Group is in the business of healing... quite literally. They specialize in high-tech wound care using placental tissue. Yes, you read that right. 🦲 Their patented PURION® process sounds more like a Marvel villain's origin story than a biotech protocol, but it's helping real-world patients and making real-world dollars.

🏥 What They Do:

MiMedx processes human placental tissue (membranes, umbilical cords, discs) to create high-value wound healing products like:

-

EPIFIX, EPICORD, and EPIEFFECT: Protective grafts used for wound care (the Band-Aids of biotech).

-

AMNIOFIX and AMNIOEFFECT: Surgical MVPs used in everything from vascular to plastic surgery.

Their tech preserves vital goodies like growth factors, cytokines, and chemokines—because nothing says healing like a soup of sci-fi-sounding proteins. 🧠

🚀 Why Are We Talking About This Now?

Because CEO Joseph Capper just bought 200,000 shares at $6.34. That’s a cool $1.27 million vote of confidence. 🤝

“Nothing screams bullish quite like a CEO buying big with his own wallet.”

Capper’s no amateur either—he previously led BioTelemetry, turning it around before selling it to Royal Philips for $2.8 billion. So yeah, he might know a thing or two.

🧹 Financial Bandages in Place

-

Q1 Net Sales: $88M (+4% YoY)

-

Adjusted EBITDA: $17M (20% of sales)

Net Income: $7M (not shabby)

-

Cash on Hand: $106M (or $88M net of debt)

Margins are slipping a bit (from 85% to 81%), but that’s mostly product mix. Overall, they’re still profitable, cash-positive, and growing.

📊 The (Kind of Meh?) Valuation:

-

P/E Ratio: 24.68

-

Forward P/E: ~23.21

It’s not screaming cheap, but it’s no nosebleed either. Think of it as moderately priced for moderate optimism.

Want to invest in an innovative biotech?

Check this out.

💸 Institutional Wrap-Up:

Institutions own about 71% of the float. Top holders:

-

Essex Woodlands: 28.2M shares (25.6%)

-

BlackRock: 10.18M shares

-

Trigran & Vanguard follow close behind

Names like State Street and Renaissance Tech also pop up on the list. Basically: it's got some smart money nibbling.

🌟 The Forecast:

-

High single-digit revenue growth in 2025

-

Long-term goal: low double-digit growth + >20% EBITDA margins

Not a rocket ship, but if they stick the landing with LCD/coding issues and product rollout (shoutout to new product CELERA™), this could be a slow-burn winner.

🕵️♂️ The Insider Takeaway:

This one might not be sexy, but sometimes boring bleeds green. You've got a seasoned CEO, solid fundamentals, new product momentum, and insider buying that screams: "I’m in."

Just remember: this isn’t a quick-fix bandage. It’s more like a long-term graft. ✨

Tags: InsiderPurchases, BiotechStocks, MDXG, HealthTech, ValuePlay, GrowthWithGrit, CEOBuyIn, EarningsBeat, MedTech

Got a thought? A tip? A tale? We’re all ears — drop it below.: